- Research suggests low savings stem from biases like present bias, where immediate rewards outweigh future gains, though economic pressures like inflation add complexity.

- Evidence leans toward mental accounting and scarcity mindset hindering savings, potentially leading to impulse spending, but individual resilience varies amid debates on behavioral interventions.

- Social factors, including FOMO from media, appear to exacerbate issues, fostering empathy for those balancing short-term joys with long-term security, without oversimplifying causes.

- While studies point to automatic savings boosting rates, controversies around over-optimism highlight the need for personalized strategies respecting diverse financial experiences.

Why Focus on Psychology?

Evidence indicates U.S. savings rates hover around 3.5-4.3% in 2026, per Federal Reserve data, far below historical averages. Psychological factors like hyperbolic discounting explain much of this, as people prioritize now over later. Start small: Automate transfers to combat biases.

Common Barriers

Present bias, loss aversion, and status-seeking often derail efforts. For instance, dopamine from spending overshadows saving’s delayed rewards.

Overcoming Impulse Spending Anchor bias ties us to first prices seen, fueling overspend. Counter with budgets.

Building Habits Celebrate wins to rewire guilt; seek support for fear.

The Hidden Mind Games: Unpacking Why Saving Feels Impossible

Ever caught yourself scrolling through online deals, adding to cart, and thinking, “I deserve this”? In 2026, with U.S. savings rates dipping to around 3.5% as per recent Federal Reserve reports, millions grapple with this impulse. But it’s not just willpower—psychology & human behavior play starring roles, weaving biases that make stashing cash feel like climbing Everest. Drawing from behavioral economics, let’s explore why Americans struggle to save, blending stats, expert views, and fresh angles like AI’s role in amplifying temptations.

Comparing Economic vs. Psychological Hurdles

Savings struggles aren’t solely economic; psychology amplifies them. Here’s a table contrasting factors, based on insights from sources like the Poverty Action Lab and Brigham Young University studies:

| Factor Type | Economic Examples | Psychological Examples | Impact on Savings |

|---|---|---|---|

| External Pressures | High inflation (2.7% in 2025), rising costs (24.3% since 2020) | Present bias: Overvaluing immediate rewards | Economic squeezes budgets; psychology justifies spending “relief” |

| Income-Related | Low wages not matching inflation | Scarcity mindset: Short-term focus | Stagnant pay limits funds; bias ignores long-term compounding |

| Debt Dynamics | Credit card debt > savings (29%) | Loss aversion: Fear of cutting luxuries | Debt accrues interest; aversion clings to status symbols |

| Social Influences | Job insecurity (33% stress factor) | Bandwagon effect/FOMO from social media | Instability erodes confidence; FOMO drives “keeping up” spends |

This highlights how economics sets the stage, but biases like hyperbolic discounting—preferring $50 now over $100 later—steal the show. Post-pandemic, AI-curated ads intensify this, per behavioral economists, turning browsing into buying frenzies.

Financial Literacy Infographics: Personal Finance Infographics | NFEC

Key Insights: Fresh Lenses on Behavioral Traps

2026 data from Allianz surveys shows 48% feel more stressed financially than in 2025, citing day-to-day costs (54%) and low income (46%). Yet, psychology digs deeper: 32% admit spending on unneeded items, per habits polls. Let’s unpack with unique twists.

Present Bias: The “Now” Over “Later” Dilemma

Behavioral economist Brigitte Madrian notes we overweight present feelings, making future savings abstract. In 2026’s gig economy, this manifests as “treat yourself” culture amid uncertainty—why save when AI might disrupt jobs? Fresh perspective: Post-2025 inflation fatigue creates “scarcity loops,” per Mullainathan and Shafir’s research, where short-term focus trumps emergency funds (39% lack them).

- Hyperbolic discounting: Studies show people delay saving, blowing refunds as “free money” (entitlement bias).

- Tip: Automate deductions—Madrian’s field evidence shows 20-30% uptake boosts via payroll, bypassing willpower.

Mental Accounting and Impulse Traps

We bucket money irrationally: Windfalls feel “extra,” fueling spends. Capital One’s 2015 survey (still relevant) found 28% blow savings impulsively. In 2026, subscriptions drain $200/year unused, per Self Financial—decision paralysis from choices overloads cognition.

Unique insight: AI personalization exploits anchoring bias, setting high “normal” prices. One Reddit user’s story: Cutting TikTok halved binges, reclaiming hours for budgeting. Counter: 30-day “want lists” rewires guilt, per experts like Tori Dunlap.

FOMO and Status-Seeking: Social Media’s Shadow

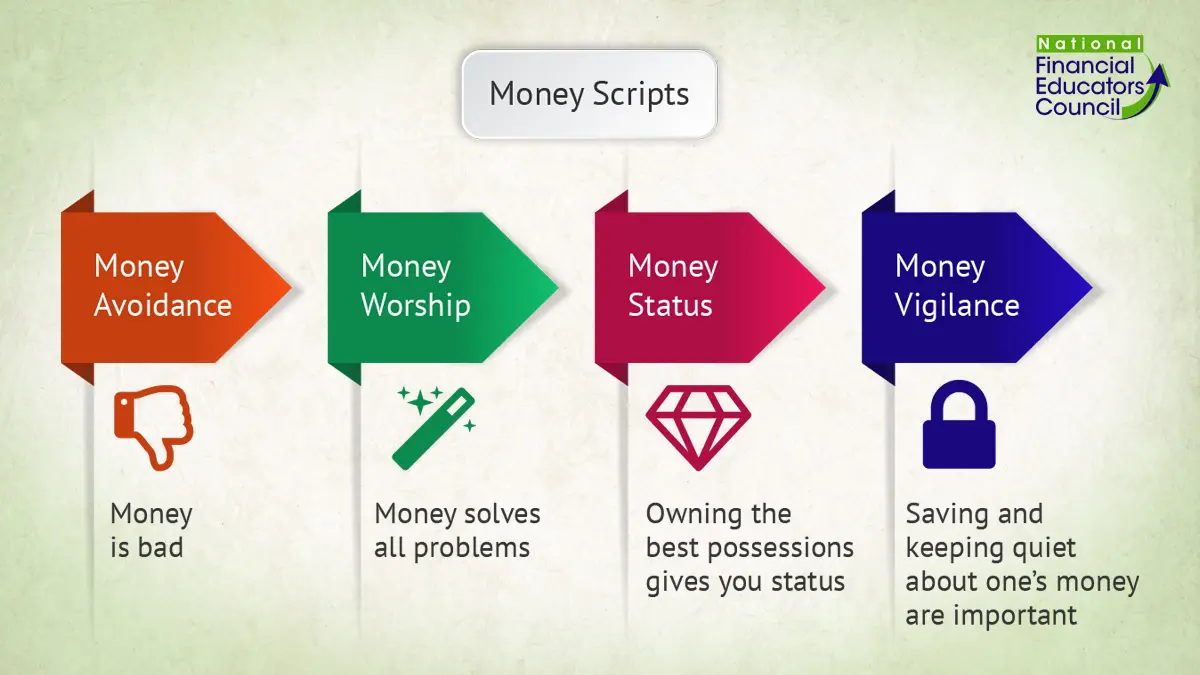

Bandwagon effect drives 44% nonessential overspend, per Intuit. Gen Z, per Bankrate, splurges on travel/entertainment despite debt. Psychology: Status vigilance (money scripts infographic) equates possessions with worth.

Fresh view: In aging America, “broke mindset” (fixed hopelessness) traps boomers ignoring 401k fees, compounding losses. YouTube analyses highlight over-optimism: “It’ll work out,” delaying AI upskilling for side income.

- Loss aversion: Cling to outdated portfolios, fearing change.

- Empathy angle: Underrepresented groups face added barriers; women derive more saving joy (58% vs. 49% men), per surveys.

A deeper table on biases:

| Bias | Description | 2026 Example | Fix Strategy |

|---|---|---|---|

| Present Bias | Immediate over future rewards | Skipping 401k for dining out | Automatic transfers |

| Anchor Bias | First price sets expectations | Overspending after seeing “deals” | Research benchmarks |

| Scarcity Mindset | Short-term survival focus | Impulse buys amid inflation | Build small emergency funds |

| Bandwagon Effect | Following peers | FOMO-driven luxury purchases | Curate mindful social feeds |

This, informed by DellaVigna and Zinman’s reviews, shows biases aren’t flaws but evolutionary holdovers—adaptable with nudges.

Understanding The Joy Of Saving Money – FasterCapital

Emotional Barriers: Fear, Shame, and the Unknown

PBS experts note fear stems from unknowns; 55% feel overwhelmed. Shame/guilt paralyzes—rewire by neutral reviews. Celebrate habits, not just goals.

Perspective: 2026’s economic shifts (tariffs, AI) amplify over-optimism, per Wharton. Yet, small wins like pausing subscriptions build momentum, addressing complacency.

Internal link: Explore digital habits wasting money for related tips.

Wrapping Up: Toward Mindful Wealth

In 2026, with rates at 4.3% projected by IBISWorld, psychology & human behavior explain persistent struggles—yet offer hope. Shift from “broke mindset” to proactive nudges; evidence leans toward automation yielding 20%+ savings boosts.

What’s one bias you’ll tackle? Share below, subscribe for behavioral tips, or join our webinar on overcoming financial fears!

Key Citations

- Nearly Half of Americans More Stressed Heading into 2026, Allianz Life Study Finds

- Americans Financial Stress 2026 Rises with Resolutions

- The No. 1 Reason Americans Are Stressed About Money Going Into 2026

- Financial Habits Americans Want To Break In 2026 To Beat The Affordability Crisis

- Nearly 1 In 4 Americans Have Zero Emergency Savings

- The Psychology of Savings: Americans Struggle to Stash Cash

- Why Do Most Americans Fail to Save for Retirement

- Americans Using Savings And Debt Amid ‘Widespread Financial Distress’

- Americans Still Fear Inflation in 2026, and Some Are Betting on Risk

- Nearly half of Americans feel financially behind as 2025 comes to a close

- Most Americans optimistic about a financial ‘resolution rebound’ in 2026

- Americans Are Rethinking Their Budgets in 2026

- I Asked ChatGPT What a 2026 Budget Needs To Lose First in a Recession

- 10 Reasons Most People Will Stay Broke In 2026

- If you have a money resolution for 2026, start here, experts say

- More Americans look to financial resolutions for 2026 as budget concerns linger

- Personal Saving Rate (PSAVERT)

- Personal Saving Rate | U.S. Bureau of Economic Analysis

- Personal savings rate – Business Environment Profile Report

- The Average Personal Savings Rate in the U.S. is 4.0% in 2026

- Behavioral Economist Explains Why So Many People Struggle To Save Money

- The Psychology of Money & Decision-Making

- Micro Investment and the Behavioral Economics of Savings

- Why is It Hard to Save Money? The Psychology of Saving Money

- Why Saving Is Hard: The Psychology of Spending

- The Role of Behavioral Economics and Behavioral Decision Making in Americans’ Retirement Savings Decisions

- Why Some People Struggle to Save Money Each Month

- SAVINGS BY AND FOR THE POOR: A RESEARCH REVIEW AND AGENDA

- How We Can Nudge Ourselves To Save More

- Mind Over Money: How Behavioral Economics Affects Your Finances

- How Behavioral Economics is Helping Banks Drive Better Money Management Experiences

- 14 Reasons Why It’s So Hard to Save Money Today

Also Read: How Americans Reduce Screen Time Without Delete Social Media