Why Smart Finance Habits Beat High Income

Most people think more income solves money problems. It doesn’t.

I’ve seen young professionals earning $90,000 living paycheck to paycheck — and college students with $1,000 saved and zero stress. The difference isn’t income. It’s Finance discipline and money management habits.

If you’re looking for:

- personal finance tips for young professionals

- personal finance tips for young adults

- personal finance tips for 20 year olds

- personal finance tips for college students

- or even personal finance tips for couples

This guide gives you practical, real-world strategies you can apply immediately.

Let’s break it down properly — not generic advice, but what actually moves the needle.

The Foundation: Money Management Tips Personal Finance Basics

Before investing.

Before side hustles.

Before crypto or real estate.

You must master money management tips personal finance basics:

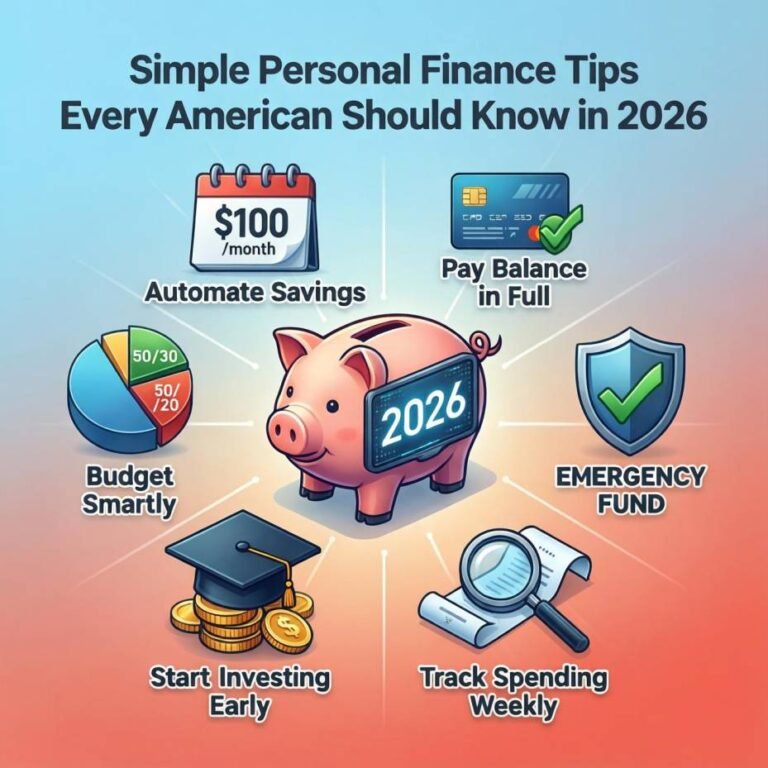

1. Know Your Real Monthly Burn Rate

Most people underestimate expenses by 15–25%.

Track:

- Fixed expenses (rent, insurance)

- Variable expenses (food, transport)

- Invisible leaks (subscriptions, small digital payments)

This single exercise creates instant awareness.

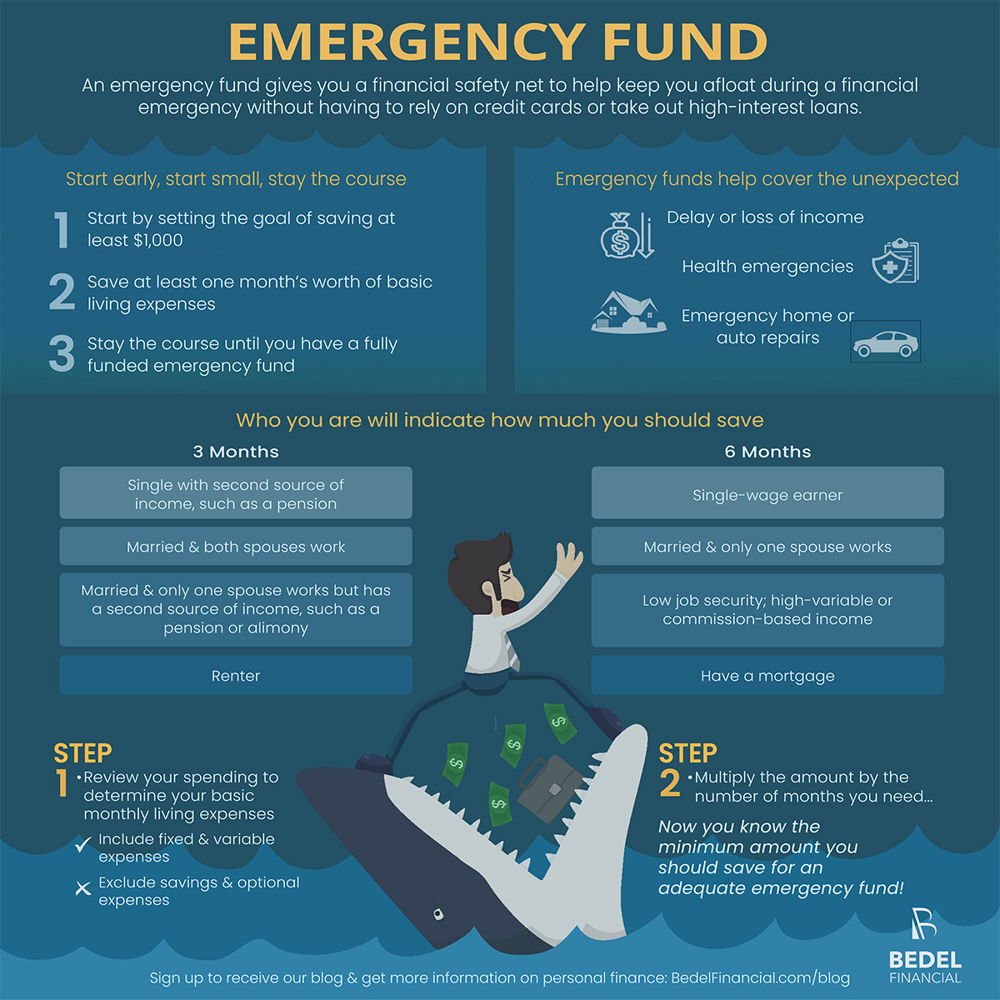

2. Build an Emergency Buffer First

In the United States, the Federal Reserve regularly reports that many Americans struggle with emergency savings.

Whether you’re following personal finance tips United States style or personal finance tips UK budgeting structures — one rule is universal:

3–6 months of essential expenses in liquid savings.

For 20 year olds or students, start with $1,000.

For couples or professionals, aim higher.

Comparison: Financial Priorities by Life Stage

Here’s where most blogs fail — they give the same advice to everyone.

Finance advice must match your life stage.

| Life Stage | Main Focus | Risk Level | Strategy |

|---|---|---|---|

| College Students | Avoid debt traps | Low income | Budget + side income |

| 20 Year Olds | Skill growth | High growth | Invest early |

| Young Professionals | Asset building | Medium | Automate investing |

| Couples | Alignment | Shared risk | Joint financial goals |

| Women (Career Growth) | Wealth protection | Long-term | Retirement focus |

Now let’s go deeper.

Personal Finance Tips for College Students

If you are in college, your biggest asset is time.

Top moves:

- Avoid high-interest credit cards.

- Use student discounts strategically.

- Learn investing basics before earning big money.

- Build credit responsibly.

These early personal finance saving tips compound massively later.

Personal Finance Tips for 20 Year Olds & Young Adults

Your 20s are your financial launchpad.

Here are the top personal finance tips for this stage:

✔ Invest Before You Feel Ready

Start with index funds or retirement accounts.

Even $100/month builds momentum.

✔ Increase Income Before Cutting Coffee

Skill stacking beats extreme frugality.

✔ Avoid Lifestyle Inflation

First raise? Save half. Upgrade later.

These are some of the best personal finance tips for saving interest long term — because compound interest works best early.

Personal Finance Tips for Young Professionals

This stage is dangerous.

Income increases.

Expenses quietly rise.

Savings stay flat.

If you’re a young professional:

- Automate investing before lifestyle upgrades.

- Negotiate salary — it compounds for decades.

- Track net worth quarterly.

Many personal finance tip blogs ignore salary negotiation — but a $5,000 raise invested annually can mean hundreds of thousands over time.

Personal Finance Tips for Couples

Money fights break relationships faster than almost anything.

Here’s what works:

Have Monthly Money Meetings

Not emotional discussions — structured reviews.

Define:

- Shared goals

- Separate discretionary budgets

- Long-term investments

Strong couples use structured systems — not assumptions.

These are essential personal financing tips for building wealth together.

Personal Finance Tips for Women

Women statistically live longer and often experience career breaks.

Key strategies:

- Prioritize retirement contributions early.

- Build independent credit history.

- Maintain emergency savings in your own name.

Financial independence equals life flexibility.

Weekly Personal Finance Tips System (Simple Habit Strategy)

Instead of overwhelming yourself, use this weekly rotation:

Week 1: Track spending

Week 2: Reduce one expense

Week 3: Increase income

Week 4: Review investments

Repeat monthly.

This turns random advice into structured weekly personal finance tips you can actually implement.

Regional Angle: Personal Finance Tips United States vs Personal Finance Tips UK

While principles remain similar, systems differ.

| Factor | United States | UK |

|---|---|---|

| Retirement | 401(k), IRA | Pension schemes |

| Healthcare | Private insurance | NHS |

| Credit Score Impact | Extremely high | Important but less dominant |

Adjust strategy based on your country’s system.

Personal Finance Tips Texas Newsletter Angle

If you’re targeting a regional audience (like a personal finance tips Texas newsletter), consider including:

- Texas property tax insights

- No state income tax advantage

- Real estate investing trends in Texas cities

- Small business financing in Texas

Localized finance content ranks well in search and builds authority.

Best Personal Finance Tips for Saving Interest

Interest works two ways:

✔ It builds wealth when invested.

✘ It destroys wealth when attached to debt.

Top rule:

- Pay off high-interest debt before investing aggressively.

A guaranteed 18% credit card payoff beats most market returns.

Visual Breakdown: The Wealth Order

📊 Step 1: Emergency fund

📊 Step 2: Employer match retirement

📊 Step 3: High-interest debt elimination

📊 Step 4: Long-term investments

📊 Step 5: Advanced investing (real estate, business)

Simple. Repeatable. Effective.

Key Insights Most Personal Finance Tip Blogs Miss

- Income growth > extreme budgeting

- Automation beats motivation

- Net worth tracking changes behavior

- Small consistent investing beats big random investing

- Financial clarity reduces anxiety

Finance isn’t just math.

It’s psychology.

Conclusion — Finance Is a Skill, Not a Salary

The best personal finance tips are not flashy.

They are consistent.

Whether you’re:

- A college student

- A 20-year-old just starting

- A young professional

- A couple building wealth

- A woman planning long-term independence

- In the UK, United States, or Texas

The principles stay the same:

Spend intentionally.

Save automatically.

Invest consistently.

Increase income strategically.

Also Read: 10 Personal Finance Tips Every American Should Know But Most Ignore in 2026